Cost of Living Crisis: Homeowners Stretch Mortgages to 35 Years

During the pandemic, the government’s incentive to remove the stamp duty levy on all properties up to £500,000 sparked a rush for buyers to purchase larger and more expensive properties by taking out home loans for extended periods. There is a prediction from experts that the cost of living increases we are currently experiencing could be the result of a surge in 35-year-plus mortgages.

The stamp duty tax relief meant that buyers could save up to £15,000 when buying a new home before it was tapered down in June 2021 and finally stopped in September 2021. Data reveals that the number of 35-year-plus mortgages increased significantly towards the end of both of these periods.

A typical mortgage term is 25 years, which is the time period over which a home loan is paid. Figures released by Quilter, a wealth management firm, show that in June 2021, there were 35,046 mortgages sold with payment terms of 35 years or more. This equates to an increase of 209% when compared to the previous June.

September 2021 showed a growth of 73% in longer-term mortgages, rising from 16,066 in September 2020 to 28,112 the following year.

Data shows that buyers have been stretching themselves financially in order to buy at a time when house price hikes were at a high, with the average home cost increasing by 13.2% in the year to June 2021.

The reason most will have opted for a 35-year-plus mortgage was to meet their monthly repayments on properties that would be too expensive over a shorter term. By spreading the loan, monthly payments are reduced.

David Hollingworth, associate director at broker L&C Mortgages, says that the longer-term mortgage has been a growing trend in recent years.

‘We do know that there has been an increase in borrowers structuring their mortgage over longer terms for a number of years now, often driven by high house prices,’ he says.

‘Taking a longer-term will help give buyers a bit more flexibility in their monthly budgeting by reducing the monthly payments on a repayment mortgage.

‘That helps with affordability and can be a comfort to first-time buyers taking their first step on the ladder who may want some breathing space in the early stages.’

But will the ever-increasing cost of living make longer-term mortgages more common than not? With increased monthly outgoings and house price increases (11% increase to the end of March), it is expected that more buyers will take this option.

Mortgage interest rates are also on the rise, leading to many homeowners looking for ways to decrease their monthly mortgage burden by remortgaging their property using a longer-term mortgage. Longer-term home loans generally allow the buyer to lend more money so that they can also buy a bigger or better property.

Martijn van der Heijden, chief financial officer at mortgage broker and lender Hibito, said: ‘For some people, the impact of inflation will take a big toll on their monthly outgoings.

‘We’ve had inquiries from customers wanting to remortgage to change their term from 20 years remaining to 30 years remaining to reduce their monthly repayment amount.

‘With some incurring national insurance tax rises, alongside frozen income tax thresholds and frozen student loan repayment thresholds, we could see more customers looking to extend their mortgage terms to make their monthly repayments lower.’

There are some risks associated with taking out a long-term loan. You will need to carefully consider the interest rates being offered.

‘Other than the obvious appeal of lower monthly payments, there’s not much to back the case for longer mortgage terms,’ stated Hollingworth.

‘It will come with a cost in the longer run in terms of the total interest payable over the life of the mortgage.

‘Paying the mortgage back more slowly means that more interest will be charged, and that can amount to tens of thousands of pounds.’

The fact that the extension of the loan term could take some people right into retirement is something that should be given consideration.

Hollingworth says: ‘A long term won’t always be an option, as lenders will consider your age at the end of the mortgage term and won’t simply allow a 40-year term to be taken time after time.’

Another disadvantage is that it will slow down the pace at which a homeowner can gain equity in the property.

‘It’s also worth bearing in mind that paying off the mortgage more slowly will mean that the mortgage represents a higher proportion of the property value for longer, so it might not allow a drop into lower loan value bands as soon,’ says Hollingworth.

‘If prices are climbing, that may not be a problem, but if the market is flat or falls back, then it could limit options.’

At the end of the day, opting for a 35-year-plus mortgage will help to alleviate the current escalation of household bills and the cost of living, but may in the long run result in thousands of extra pounds being spent.

Cost of Materials and Labour Spells Disaster for Self-Build Boom in the UK

It’s everyone’s dream to have a home built specifically for them. Designed with lifestyle and taste in mind, home builds have proved to be very popular over recent years.

More recently, spiralling inflation and shortages in materials and labour, alongside the war in Ukraine, have caused the costs of building a new home to skyrocket. With most of the most commonly used materials used for construction rapidly increasing in price, developing and building properties are set to take a downturn across Britain.

Neil Rogers of Honeywood Joinery, a carpentry business in Newcastle-under-Lyme, says: ‘I was told by my local merchants that if you’re pricing up a job and it’s longer than a month away, add another 15 to 20 per cent for more timber inflation.’

With the announcement from British Steel of a 25% hike in prices on some of their products, it isn’t surprising that developers and individuals are being more cautious when costing up development projects. Cement companies have reported an eleven per cent reduction in the production of cement, signifying a lowering in demand.

According to data from the National Federation of Roofing Contractors, around 60% of roofing firms have increased their charges.

Figures provided by the Department for Business, Energy, and Industry Strategy show that there has been a massive 21% increase in general materials in the last year. This data was calculated before the onset of the Ukraine war and the energy crisis, meaning prices can be expected to continue on an upward trajectory for some time to come.

So, whether you are doing a self-build or just a modest extension, price rises are sure to make your eyes water.

According to a price comparison site, roof tiles have risen by a whopping 24%, underfloor heating by 15%, and loft conversions by 20% over the last 12 months. Plywood is 44% more expensive, and uPVC has soured by 42%.

The most shocking of all price increases has to be for rolled sheet joists, which have risen by an unbelievable 82%.

Mike Fairman, the chief executive of Checkatrade, said: ‘The current global raw material shortage has had a profound impact on the UK trade and construction industry.

Soaring demand, the impact of Brexit, continued pandemic recovery, and shock factors like forest fires in North America are all reasons behind the shortages.

These massive increases are leading to a rapid decline in the growth of the self-build market. Analysis by estate agency Savills reveals that between 7 and 10% of all homes built in the UK are self-built, equating to around 130,000 per year. The government has plans to increase this to between 30,000 and 40,000 annually and has requested that councils keep a register of self-builders who are looking to purchase plots to develop. The aim is to use spare land that can be developed and offered to those on the register; however, the uptake has been somewhat patchy.

But dreams of your perfect self-build do not need to be forgotten necessarily. Instead, it is worth considering options to keep costs down to a minimum for new builds and extensions.

Getting quotes for labour and materials before the build starts will help to realistically cost the project. Also, bear in mind that the design may cause additional costs; for example, an open-plan design will most likely need load-bearing steel, which is one of the materials that has seen the largest price increase.

Purchasing an ‘off-the-shelf’ home will likely save you some money; in other words, considering a kit-built house is an option to keep costs down. The advantage of this is that buyers are paying a one-time payment for the design, including all the materials, fixtures, and fittings.

One bit of positive news is that the government has scrapped VAT for all materials intended to make homes and properties more environmentally friendly and energy efficient.

Average House Prices in Scotland Hit a New All-Time Record High

First-time buyers looking to get on the Scottish property ladder could be facing an uphill struggle this year as average property prices reach new record highs. For the seventh time within the past 12 months, the average market value of a home in Scotland has broken all previous records.

New data from the Walker Fraser Steele House Price Index indicates that the average price of a home in Scotland hit £218,702 in February 2022, an increase of £16,600 compared to February 2021.

On a monthly basis, Scottish house prices were up 1.5% in February compared to the month before, amounting to a one-month increase of £3,200 on average. This is the largest monthly increase recorded since August last year, with average house prices increasing in 30 of Scotland’s 32 local authority areas over the past year.

Only two areas recorded slight reductions in price over the past 12 months, which were Clackmannanshire and Aberdeen City. Meanwhile, the Orkney Islands saw the biggest gains of all, where average house prices increased by a huge 28.6% since the same time last year.

Competition remains ferocious

Senior housing analyst at Fraser Steel, John Tindale, highlighted similarities in the real estate sectors of England and Wales. Last month, all nine English and Welsh regions recorded all-time high average property prices, with Wales achieving the strongest annual growth rate of 8.9%.

“There is still high demand for such homes, but supply is limited, so there continues to be strong competition for the properties that do come on the market, with resultant price increases.”

Elsewhere, the regional development director at Walker Fraser Steele, Scott Jack, said that the way Scotland’s real estate sector has returned to strength was highly impressive.

“As a piece of context, in February this year, all the regions in England and Wales established new record average house price levels, but it is fair to say that the Scottish property market has robustly withstood one of the most seismic events in living memory in the past couple of years,” he said.

Shifting priorities and changing lifestyles

Analysts continue to cite the ongoing home-working trend as the biggest single contributor to explosive competition in the UK’s housing market.

Meanwhile, record-high rent yields across the country are motivating landlords and investors to expand their portfolios, putting even greater strain on the sector’s limited available inventory.

Even as the gradual return to the office accelerates, lifestyle changes brought about by the pandemic are likely to continue altering the public’s priorities in the long term. All of which is likely to sustain the housing market’s blistering performance indefinitely as demand continues to outpace supply by a clear margin.

Landlords and Homeowners to Get Tax Relief to Improve Energy Efficiency

Following the Spring Statement this month by the Chancellor of the Exchequer, Rishi Sunak, landlords and homeowners were given the good news that all materials used for improving energy efficiency in their properties would now be VAT-free for the next 5 years, down from the previous figure of 5%.

This reduction in tax represents an estimated saving of £1,000 upfront and will further result in lower energy bills, saving around £300 per year per household. The announcement comes at a perfect time, particularly for landlords who are required to meet new EPC regulations to upgrade their properties and make them more environmentally friendly.

The new EPC (Energy Performance Certificate) regulations stipulate that landlords must increase the rating of their properties to the minimum of a C rating by 2025. This applies to all new tenancies and will be followed by all tenancies by 2028. This could add up to a large bill for landlords, who will be required to make any changes needed to reach the required rate, so the zero VAT on materials will help to keep costs down.

The 5% saving on materials will give landlords an opportunity to reduce their outgoings during periods when their properties are vacant and will in turn help tenants by reducing their energy costs, which will be gratefully received considering the recent increases in rental prices.

Rental rates have increased at their highest annual rate for more than five years, hitting the highest growth seen within the last year. The ONS (Office of National Statistics) has released data showing a 2.3% increase in prices in the private rental sector, the highest seen since December 2016.

The largest rental growth was recorded in the East Midlands, with an increase of 3.8%. London showed the lowest rental price hike, increasing only 0.2%, primarily due to the change in working habits, with many people opting to continue to work from home post-pandemic, according to the ONS. Excluding London, the rest of the UK saw rental prices increase by 3.2% in the last 12 months, up slightly from 3% in the year to January 2022. Looking at each individual country, Scotland leads the way with a rise of 2.6%, followed by England at 2.1% and Wales at 1.4%.

Research conducted by Rentd revealed that the average earnings of tenants fell far below the affordability level for rental prices across all regions of all five nations. This is calculated by looking at the average earnings of a typical renter and using a benchmark of two and a half times the average rental rates. The report found that the average annual wage for those who rent in the private sector was 12% lower than the wider average, with an average income of £28,116.

Across the UK, the average rental price is £968 per calendar month (£11,616 per annum). A tenant would need to have a salary of at least £29,041 to comfortably be able to afford this rental rate. This is a shortfall of £925 when calculating using the 2.5 times wage affordability formula.

With inflation spiralling and the cost of living rapidly increasing, many renters’ dreams of homeownership are becoming unreachable, putting even more pressure on the private rental sector to find more housing stock. The demand for quality, affordable rental properties is on the increase, with both landlords and tenants needing support through these turbulent times.

Reducing Borrowing Costs with New Equity Release Rule

Homeowners, who have taken advantage of equity release finance, are now able to make additional partial payments without any charges or penalties in a bid to reduce borrowing costs.

Although this is a feature already offered with some later-life lending products, as of March 28th, the Equity Release Council announced that it will be mandatory for lenders to include this feature with all equity release finance products.

The ability to make extra payments will result in homeowners reducing the impact of compound interest later down the line and decreasing the overall cost of equity release.

Equity Release Finance is a way of releasing the tied-up cash in your home. It allows for borrowing against the equity in your house without being required to make any repayments. The loan is repaid when the borrower either moves into residential care or passes away. To be eligible for equity release, you must be over 55 years old.

This new rule will allow the homeowner to make payments as and when they wish, thereby reducing the amount that the lender will be repaid when the time comes.

The Equity Release Council, which announced the news regarding the new product safeguard on Monday, stated that over the next decade, a total of £39 million in combined savings can be achieved, with further figures predicted to be a whopping £99 million in expected savings over the next twenty years.

Data shows that, in 2021, more than 125K part payments towards equity release plans were made without penalty.

Jim Boyd, CEO of the Equity Release Council, said: “The right to remain in your home for life, with no requirement to make ongoing repayments and no threat of repossession, has been central to the appeal of equity release since 1991 and remains a core pillar of the modern market.

“Our new product standard adds to this by ensuring people have the freedom to reduce their borrowing if circumstances change.

“It enables equity release customers to mitigate the effects of compound interest and reduce their borrowing costs in later life, which we know is often one of their main concerns.”

This latest product standard, released and enforced by the Equity Release Council, sets out the following parameters:

It gives the homeowner the right to live on the property for the rest of their lives; they will also have no obligation to make any payments until they go into full-time care or pass away.

The interest rate is capped or fixed for life. The rate of interest will never change, even when base rates change.

No negative equity guarantee: The debt will never be more than the home is valued at, meaning that relatives will not be burdened with any funds owed to the lender.

The right to move the loan: Providing it meets the criteria, the loan can be moved to a different property.

Jim Boyd added: “Equity release today is a flexible financial planning tool for a range of scenarios, from gifting to family to supporting better living standards over longer lives in retirement.

“Consumers should always use a Council member to explore their options and alternatives to equity release, to benefit from product protections and expert advice, and to decide if it is right for them.”

Bridging Loans for Property Development: How Does it Work?

Specialist development finance is a popular choice for property developers and construction companies, providing prompt access to significant sums of money for extensive and ambitious projects.

However, there are scenarios where a bridging loan for property development could be a better choice. Unlike development finance, bridging loans are issued in the form of a single lump sum. Not released in a series of stages as the project progresses. In addition, qualifying for a bridging loan can be fairly straightforward, whereas development finance is offered exclusively to established property developers.

But how does a development bridging loan work, and what are its key features? More specifically, what makes a bridging loan for property development a better choice than a standard commercial loan or mortgage?

Typical applications for property development bridging loans

A bridging loan can be used for any legal purpose, with few restrictions as to the potential applications for the funds. Some of the more common uses of property development bridging loans are as follows:

- To pick up low-cost properties at auction and to fund the subsequent renovations required.

- To purchase a plot of land quickly and beat rival bidders to the punch.

- To commence and complete a project as quickly as possible when time is a factor

- To fund any kind of property development project as a new or experienced developer.

Property development bridging loans can also be a useful facility for subprime applicants who would otherwise be unable to qualify for a conventional property loan or mortgage.

How does a development bridging loan work?

A development bridging loan is a strictly short-term facility designed to ‘bridge’ a temporary financial gap. Ideal for time-critical purchase and investment opportunities, a bridging loan can be arranged and issued within the space of a few days.

Repayment typically takes place six to 18 months later, in the form of a single lump-sum payment inclusive of rolled-up interest. Monthly interest applies at rates as low as 0.5%, negotiable in accordance with the size and nature of the loan taken out.

Maximum loan values are tied to the assessed value of the assets used to secure the loan, which is typically the home or business property of the applicant. Lending policies vary, but most bridging finance specialists are willing to offer anything from £50,000 to more than £10 million.

How much deposit do I need for a development bridging loan?

Technically speaking, there is no specific deposit requirement for a development bridging loan. Most lenders are willing to offer loans with a maximum LTV of 70% to 80%. This would therefore mean that the investor would need to cover the other 30%/20% of the costs, but not in the form of a deposit in the conventional sense.

A higher loan-to-value ratio can sometimes be negotiated, often up to 100% LTV. An alternative option is to take out a bridging loan with an LTV of 70% or 80% and use a second- or third-charge loan from a separate provider to cover the additional costs.

As all development bridging loans are bespoke agreements between the issuer and the borrower, terms and conditions can be negotiated to suit all requirements and preferences.

Getting the best deal on a development bridging loan

All bridging loan applications are assessed on their individual merit, highlighting the importance of presenting a convincing case.

Specifically, there are four factors that will determine the competitiveness or otherwise of the loan you are offered:

- Your exit strategy: Your lender will expect to see evidence of a viable exit strategy, i.e., when and how you intend to repay the loan. For example, by selling the property you plan to purchase after renovating it, you raise the capital needed to repay the loan, resulting in additional profits for you to retain.

- Available assets: All property development bridging loans are secured against viable assets – usually residential or commercial property. However, some lenders are willing to accept other assets of value, ranging from vehicles to business equipment to intellectual property to company shares.

- Credit history: Poor credit will not necessarily count you out of the running for a competitive bridging loan. Most lenders are willing to work with subprime applicants, but a good credit history could help you qualify for the best possible deal.

- Experience: Understandably, lenders will usually reserve their best deals for applicants with an established track record in the property development sector. The more experienced you are, the more likely you are to qualify for a competitive bridging loan.

With each of the above, your broker will provide the independent support and advice you need to present a convincing case to your preferred lender.

Your broker will also negotiate on your behalf to ensure overall borrowing costs are kept to the bare minimum.

Price of Mortgages Predicted to Be £800 More Per Annum Than in October 2021

According to mortgage advisor L&C, people looking to remortgage their homes are expected to pay, on average, an additional £800 each year when compared to just five months ago.

The analysis was based on several parameters, using the example of a homeowner who had 40% equity in their property and was looking to take on a 2-year fixed-rate mortgage over a 25-year period on a mortgage of £150,000.

Figures provided by the Bank of England showed that applications for remortgage products rose in the last quarter of 2021 in proportion to overall lending. Market experts indicated that homeowners remortgaging the properties were hoping to grab a good deal before interest rates rose further, as they are predicted to do in the coming months.

Interest rates from major lenders were used by L&C, which were averaged out to create the analytic report.

The data showed that in October 2021, with interest rates at an all-time low, borrowers would be paying a little more than £557 per month on a 2-year fixed-rate mortgage deal.

If the same homeowner were to remortgage now, they could expect to pay around £627 per month, which will equate to an extra £70 monthly, which is approximately an additional £840 per year.

In some instances, good mortgage deals are only made available to borrowers for a very short period of time, often just days, and are then removed from the market. What homeowners need to realise is that they can apply for a new mortgage up to six months prior to the end of their current mortgage arrangement.

L&C also stressed that offers from lenders are typically valid for 3 to 6 months, giving the borrowers “Rates are moving quickly, though, and deals rapidly come and go, often only lasting a matter of days before being replaced with higher rates. Sufficient time to make an application despite the fact that an ERC (early replacement charge) may stay in place for several months.

Associate director at L&C Mortgages, David Hollingworth, commented: “Mortgage rates have been shifting rapidly as lenders are forced to adapt to the impact of market expectations of higher rates on their funding costs.

“The sheer pace of change is something that could take borrowers by surprise, especially when the cost of living and other outgoings such as energy are already rising too.

“Fixed rates are still at historically attractive levels, so borrowers should review their current deal to make sure that they are on the best deal and protecting their position, especially against a backdrop of rocketing outgoings and further potential increases in the base rate.

“Borrowers can lock in at a current rate up to six months ahead, giving them the chance to review well ahead and ensure a smooth switchover when their current deal ends. That could help them get ahead of any further rate rises.”

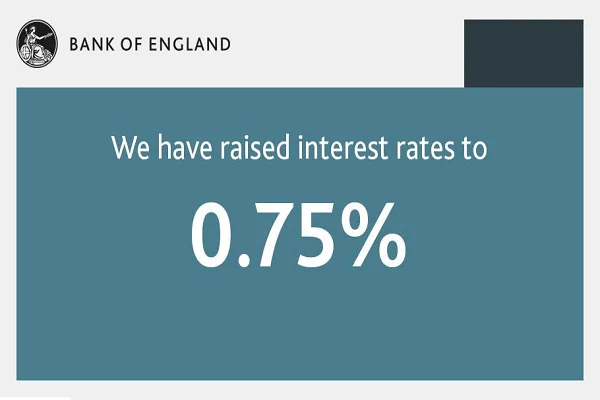

Base Rate Rise to 0.75% Expected from the Bank of England as Inflation Further Escalates

The Bank of England is under increasing pressure to raise interest rates as the Russian attack on Ukraine escalates. Despite the conflict bringing a high level of economic uncertainty to the UK and warnings from the Chancellor of a turbulent future, base rates are expected to rise to 0.75% this week. This, coupled with the expectation that base rates will go as high as 2% by the end of the year, is a real fear in UK households, with the cost of living going up every day.

In February this year, the Bank of England predicted that consumer price inflation would hit its highest level in April at 7.25%, coinciding with the expectation that gas and electricity bills would go up by a whopping 54% when the price cap increased.

These predictions have now been adjusted and are expected to rise to as much as a 9% inflation rate in the coming months. The rise in interest rates is an attempt by the Bank of England to fight the increasing cost of living, making borrowing far more expensive than previously.

With inflation currently at a 30-year high of 5.5% and expected to rise to more than four times the bank’s 2% target, it is imperative that the bank finds a way to get inflation under control.

The invasion of Ukraine by Russia has placed additional pressure on the Bank to increase the base rate.

The nine members of the Monetary Commission are predicted to increase the rate on Thursday of this week (17th March) from the current rate of 0.5% to 0.75% in the battle to gain control over the economy and inflation.

This indicates a third rise in the base rate since December 2021 and will mean increased mortgage costs for millions of UK homeowners.

The invasion of Ukraine has resulted in skyrocketing prices for natural gas, which have risen by an incredible 60% since February, prior to Putin’s troops entering Ukraine.

Experts have stated that the rise in interest rates will not have an immediate effect on inflation in the short term and that the escalating gas and electricity costs will be a struggle for every UK household but will ultimately reduce inflation. Achieving the right balance is the aim of the Bank of England.

Research director at the Resolution Foundation think tank, James Smith, stated, “I think it’s really tough for the bank at the moment to get this right. If they go too slowly, you get an inflation shock. If they go too fast, it chokes off recovery. And then there is a recession risk on top of that.”

The fear among experts is that increasing rates to keep prices down will have a detrimental effect on an already fragile economy. Sanctions levelled at Russia are resulting in massively increased oil prices, which are hitting each and every household with fuel prices going through the roof. All of this disruption is triggering fears of a potential recession.